A Specialized Guarantee Facility for Industrial Decarbonization: The Case for a Dedicated, Pooled Risk-Sharing Instrument

This blog was originally published on Illuminem, and has been co-authored with Rhian-Mari Thomas. She is the CEO...

This blog was originally published on Illuminem, and has been co-authored with Rhian-Mari Thomas. She is the CEO...

The global transition to renewable energy systems will be mineral intensive and, under the current linear economy conditions,...

Photo by Tasha Lyn on Unsplash.

Note: CCSI submitted a response to the OECD public consultation on investment treaties and climate change that builds on the text of this piece. It is available via the Download button.

Existing investment treaties do not and cannot advance climate goals. There is a fundamental misalignment between the existing international investment regime—including its centerpiece: investor–state arbitration—and the actions needed to meet the objectives of the international climate regime and avoid catastrophic climate change. For international investment law to support climate goals, we need a wholly new regime for investment governance, not investment protection and arbitration.

Investment is crucial to achieving climate mitigation and adaptation goals. We need substantially more investment in zero-carbon sectors, such as renewable power generation (solar, wind, hydropower, and geothermal), batteries and other energy storage technologies, green hydrogen, electric transportation, and energy efficiency, while phasing out investment in fossil fuels and other high-emission economic activities. The 2022 Intergovernmental Panel on Climate Change (IPCC) report on Impacts, Adaptation and Vulnerability also stresses that investments in mitigation must be coupled with investment in adaptation and climate-resilient infrastructure to help billions in areas of growing climate risk.

International investment law should accelerate climate-friendly, sustainable investment and the phase-out of climate-unfriendly investment. Existing investment treaties and investor–state dispute settlement (ISDS) fail to do either. They were not designed to advance those goals, but to protect economic interests of foreign investors and their investments, regardless of their climate friendliness.

The 2015 Paris Agreement’s umbrella treaty, the United Nations Framework Convention on Climate Change (UNFCCC), was adopted in 1992 and entered into force in 1994—a landmark moment that emphasized the need for long-term planning for a climate-friendly future. Its ultimate objective is to stabilize greenhouse gas concentrations in the atmosphere “at a level that would prevent dangerous anthropogenic interference with the climate system.”

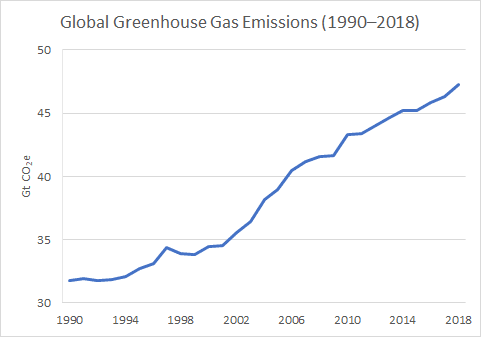

In a 1994 report—months before the first Conference of the Parties (COP) to the UNFCCC—the IPCC indicated that “the main anthropogenic sources of [carbon dioxide] are the burning of fossil fuels [among others].” The same report also estimated a carbon budget, which indicated the amount of greenhouse gases we could, starting in 1994, still emit while stabilizing concentrations at safe levels. The report stressed that “stabilization [of greenhouse gas concentrations] is only possible if emissions are […] reduced well below 1990 levels.”

The international community—including states as well as investors—has been on notice since the 1990s: to prevent disastrous anthropogenic interference with the climate system, greenhouse gas concentrations in the atmosphere must be stabilized. To do that, emissions must be reduced well below 1990 levels, which requires transitioning away from fossil energy. Yet emissions have since increased substantially as states and investors have been too slow in adjusting course.

Source: Prepared by the author based on data from ClimateWatch.

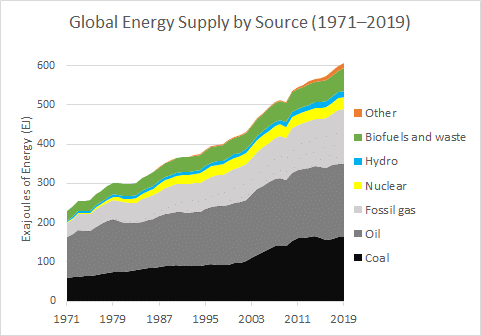

If fossil energy companies have any “legitimate expectation” since the 1990s, it is that states would take steps to phase out their sector. In the International Energy Agency’s (IEA) pathway to net-zero by 2050, “there is no need for investment in new fossil fuel supply”: “Beyond projects already committed as of 2021, there are no new oil and gas fields approved for development in our pathway, and no new coal mines or mine extensions are required.“ In the next three decades, trillions of dollars in fossil fuel assets need to be stranded to achieve climate goals, including reserves and projects that fossil and infrastructure companies have continued recklessly to develop.

Source: Prepared by the author based on data from the International Energy Agency (IEA).

States need to push more forcefully for the transition away from fossil energy in both the climate and investment regimes. It took 26 COPs for the 2021 Glasgow Climate Pact to call upon states, for the first time, to “[accelerate] efforts towards the phasedown of unabated coal power and phase-out of inefficient fossil fuel subsidies.” The climate regime still needs to toughen up language on the need to accelerate the phase-out of all fossil fuel development.

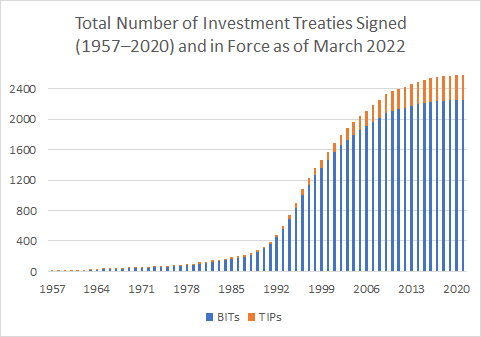

Similarly, states need to stop maintaining an investment protection regime that—among other flaws—does not even try to regulate investment or to phase out high-emission investments. Since 1994, states have concluded roughly 2000 investment treaties that are still in force. The Energy Charter Treaty (ECT) is an important one from a climate action perspective—but not the only one. All those treaties protect coal, oil, gas, and other high-emission investments that emit well beyond the carbon budget. Even if investment treaties may not have been intentionally designed to thwart climate goals, the fact that they have that detrimental effect can no longer be ignored.

Source: Prepared by the author based on data from the United Nations Conference on Trade and Development (UNCTAD).

Investment treaties and arbitration make it more costly for states to take legitimate climate action, including the phase-out of fossil fuels and the regulation of high-emitting sectors. Under the existing investment regime, companies are allowed to claim monetary compensation from states for policy measures that negatively affect the companies’ interests.

For instance, when a government takes measures to restrict oil and gas exploration or exploitation, stop the expansion of pipelines and other fossil fuel infrastructure, or phase out coal-fired power generation, investment treaties and arbitration allow investors to seek compensation for those measures. In other words, investment treaties and arbitration protect and reward investments that interfere dangerously with the climate system.

Law firms are making sure that companies are aware of this opportunistic use of investment arbitration against the public interest. As one firm advises: “Climate change litigation […] is an opportunity […] for companies exposed to certain climate-related government measures to vindicate their rights. Companies in industries most affected by states’ climate change obligations (e.g., fossil fuels, mining, etc.) should audit their corporate structure and change it, if needed, to ensure they are protected by an investment treaty. […] It is […] important to assess which treaty would best protect the company from any adverse climate-related government measures.”

Even the possibility of climate-related investment arbitration discourages policy action. Denmark, France, and New Zealand have openly admitted that they pushed back their deadlines to phase out oil and gas exploration or exploitation because of investment treaties and the fear of arbitration claims. There may well be other countries that are delaying action or lowering ambition because of the investment regime, but just not admitting it openly.

Fossil companies already account for almost one-fifth of investment arbitrations, and they won about three of every four cases initiated. Without fundamental reform, the investment regime will continue to allow fossil companies to chill climate regulation and to get states (and ultimately taxpayers) to cover losses that result from corporate recklessness.

Various reform proposals aim to make investment treaties and arbitration more climate friendly, by training arbitrators in climate science; changing how damages are calculated to avoid shifting the risk and cost of decarbonization to states; integrating climate carve-outs, exceptions, or right-to-regulate clauses into treaties; or allowing climate-related counterclaims by states. Proponents of these reforms argue that they are steps in the right direction, even if they are piecemeal approaches.

The international community should not settle for sub-optimal approaches, for three main reasons.

First, climate blindness is far from being the sole issue with the investment regime. Investment protection and arbitration constrain states’ duty and right to regulate not only in the climate policy space, but also in public health, access to public goods, protection of human rights and the environment, and the pursuit of sustainable development. States and other stakeholders have been increasingly critical of broadly worded provisions—including the promises of fair and equitable treatment (FET) and the protection of legitimate expectations, as well as protections against discrimination and indirect expropriation—that work against public-interest regulation. The member states of Working Group III of the United Nations Commission on International Trade Law (UNCITRAL) have identified various problematic aspects of investment arbitration.

Second, there is inconclusive evidence to support that investment treaties and arbitration can perform on their key expected benefits. Existing treaties neither increase the quantity or quality of foreign direct investment (FDI), depoliticize conflicts between home and host countries of investment, promote good governance reform, nor strengthen the rule of law. If a regime cannot achieve its main purposes, and its costs substantially outweigh its uncertain benefits, why put so much effort into fixing it?

Third, it is irresponsible vis-à-vis present and future generations to keep in place a knowingly flawed regime, with uncertain benefits and great known costs, in hopes that tweaking it at the margins will cause the necessary fundamental change. Given the global climate emergency, too much is at stake.

The optimal, most effective solution is to build a new international investment regime to help achieve global goals, advancing the types of investments that are desirable, supporting the phase-out of climate-wrecking investments, and preserving and strengthening states’ right and duty to take climate action and other measures in the public interest. States should move away from the existing regime, which puts profit above people and planet, by terminating or withdrawing from existing investment protection treaties and arbitration and not negotiating new ones that do not align with their climate and sustainable development objectives.

From a clean slate, the international community can design a regime that shapes and governs investment to achieve climate goals and the Sustainable Development Goals (SDGs). Investment governance treaties could contain guidance and commitments on governing investment in line with the SDGs, including climate action; establish cooperation mechanisms to address challenges in the governance of international investment, including with respect to intellectual property, technology transfer, and data; and support domestic administrative and judicial systems to facilitate investment governance and enforcement. Importantly, the regime could foster international cooperation, research and development (R&D), and financing mechanisms for climate-aligned investments, including in energy efficiency, renewable electricity, green hydrogen, batteries, recycling, and climate-resilient infrastructure. It could also affirm states’ binding commitments to phase out investment protections and incentives for fossil fuels and other high-emission investments; and create climate justice and just transition mechanisms to protect the rights and interests of those affected by zero-carbon investments.

Martin Dietrich Brauch is Senior Legal and Economics Researcher at the Columbia Center on Sustainable Investment (CCSI). He would like to thank Jack Arnold, Program Associate at CCSI, for his invaluable support in preparing this piece, and Lisa Sachs, Director at CCSI, for her invaluable input. This piece is based on the author’s intervention at the online event Climate Action beyond the Climate Change Regime: The Role of Human Rights and Investment Law, hosted on February 7, 2021.