Primer on International Investment Treaties and Investor-State Dispute Settlement

A printable version of this primer is also available here. French, Spanish, and Khmer versions are also available.

The illustrations used in this primer were developed in collaboration with Picture Human Rights. You can download the illustrations and use them in accordance with their license at this link.

[Updated as of January 2022]

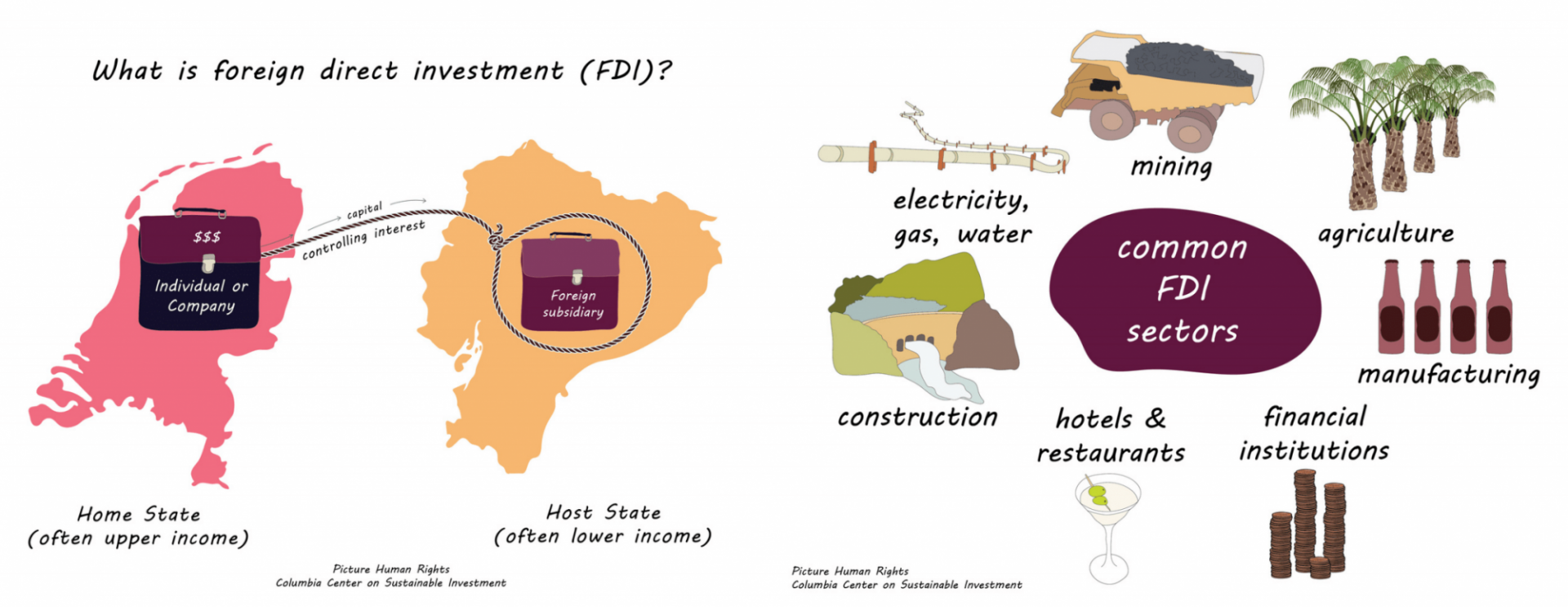

What is Foreign Direct Investment (FDI)?

FDI occurs when an individual or corporation in one country (“home state”) sets up or buys all or a significant part of a company that is incorporated in a different country (“host state”). Companies invest abroad to access land-based resources including mining, more affordable labour for instance in manufacturing, and new markets, among other reasons. Many countries seek to attract FDI in order to realize benefits in the form of tax revenues, technology transfer, jobs, and other economic linkages. The figure below illustrates the concept of FDI, as well as some of the sectors and industries into which it flows.

Governments, intergovernmental organizations, and the media report annually on FDI data—how much governments are receiving, overarching trends, and so on. It is important to note that there may be significant flaws in this data. A 2019 IMF report noted that almost 40% of global FDI may be “phantom investment”, or investment into “corporate shells” with “no substance, and no real links to the economy”. This paints a very different picture about global FDI flows than could be inferred from most available reports.

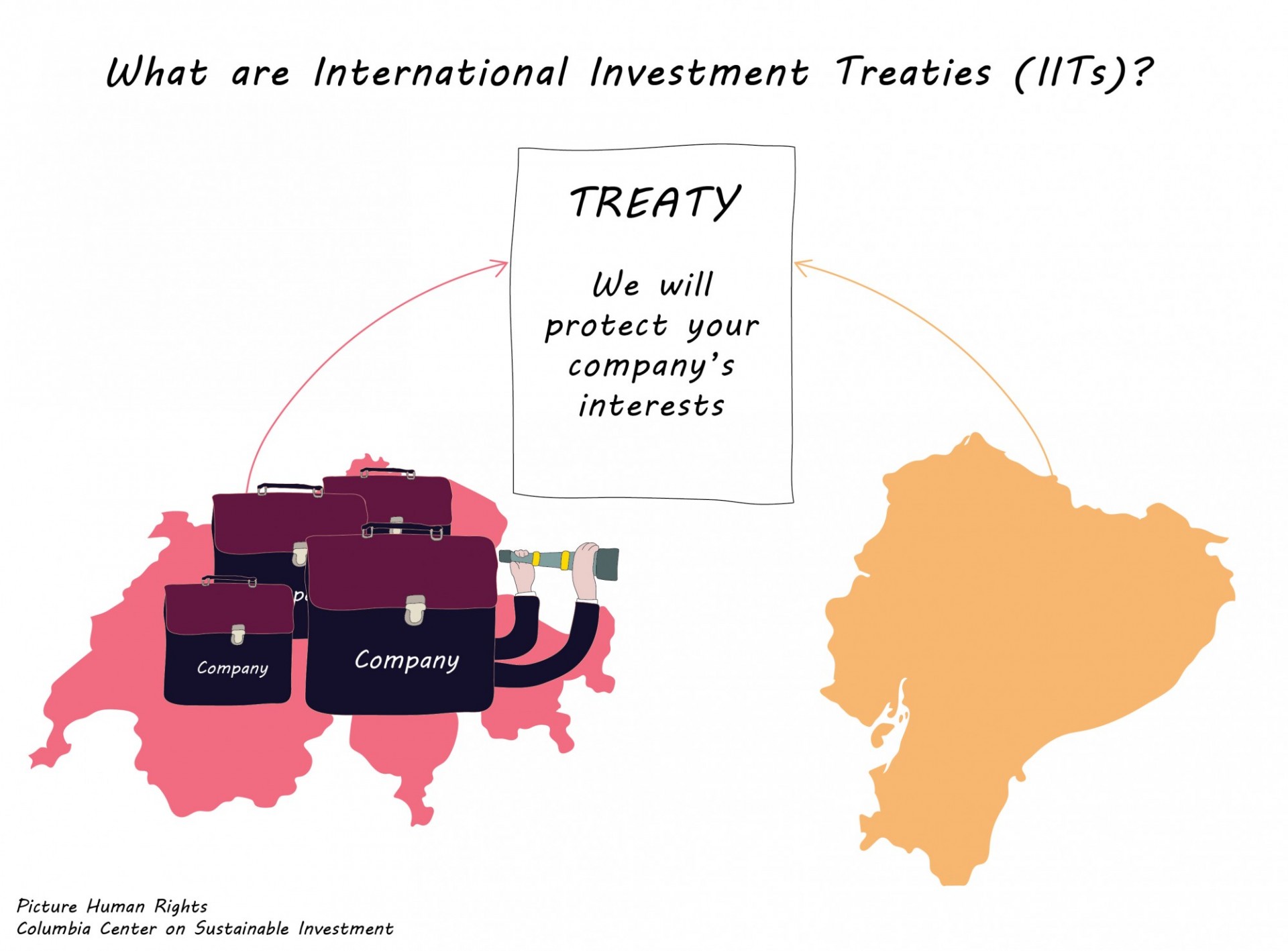

What are International Investment Treaties (IITs)? IITs (also called International Investment Agreements, or IIAs) are bilateral or multilateral treaties that commit state-parties to afford specific standards of treatment to foreign investors from the other state-parties. These treaties grant foreign investors certain protections and benefits, including recourse to Investor-State Dispute Settlement (ISDS) to resolve disputes with host states. Over 3,300 agreements have been concluded worldwide.

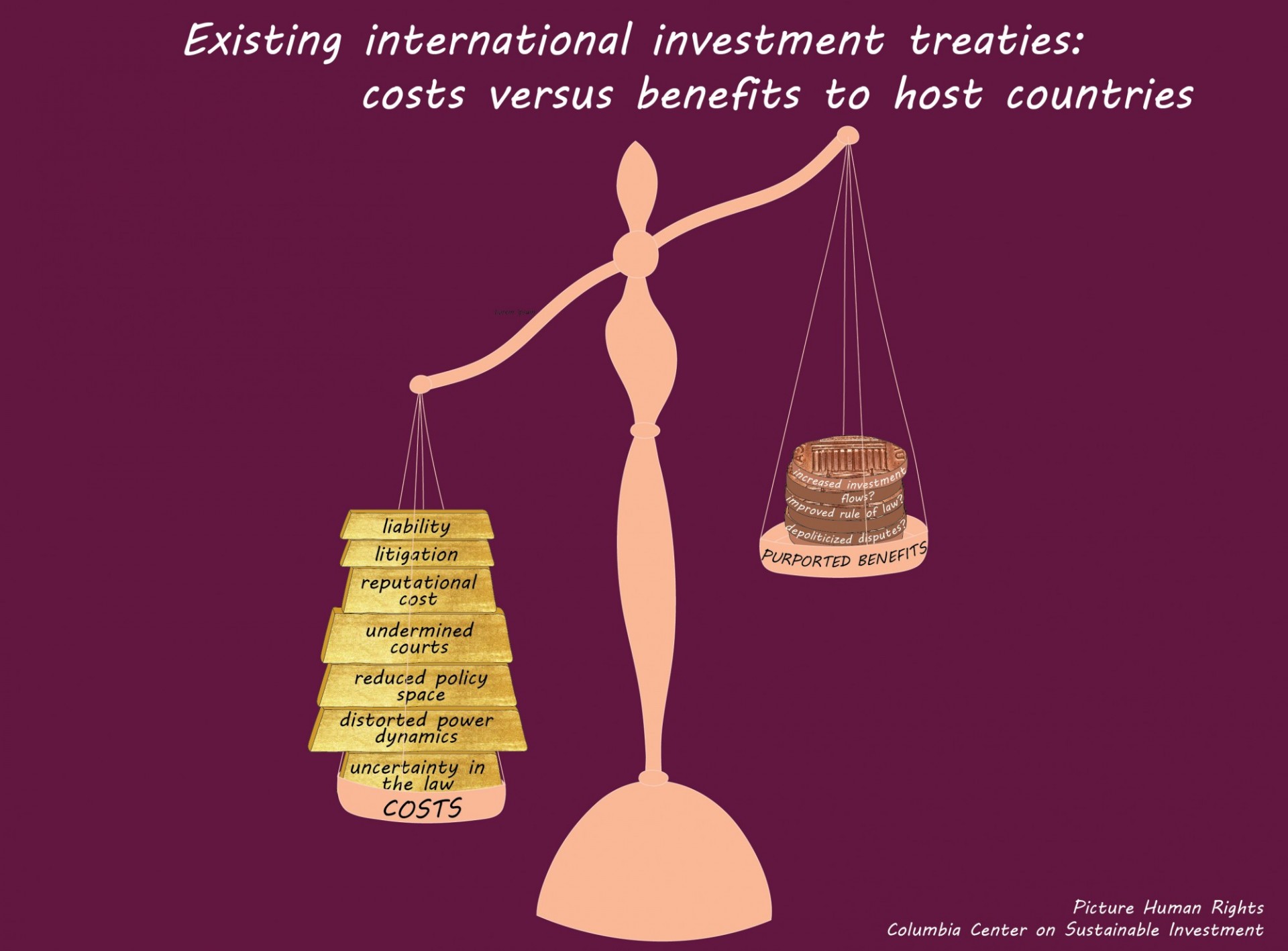

Why do countries sign IITs? States often sign IITs based on the assumptions that (1) investment protections and privileges will promote investment flows, (2) those investment flows will promote sustainable economic development, and (3) that the development benefits of IITs outweigh the costs for the state and its citizens. Proponents of IITs also allege that the treaties, including their dispute settlement mechanism, depoliticize disputes between investors and states, and between the state parties, and promote the rule of law.

Empirical evidence, however, does not show that IITs actually stimulate new investments, let alone demonstrate whether those investments in fact benefit host (or home) countries, or whether the benefit of any new investment outweighs the costs that may be associated with investment treaties (e.g., in the form of lost regulatory space, costs of defending disputes, and costs of paying adverse awards). A 2020 meta-analysis of 74 empirical studies found that the effect of IITs on FDI is “so small as to be considered zero.”[1]

There are similar doubts about IITs’ contributions to their other purported aims – namely depoliticization of disputes and advancement of the rule of law. Accordingly, many question whether IITs are tailored to deliver on their stated objectives effectively and efficiently and whether those stated objectives align with countries’ goals; and many worry about the costs that IITs may impose on states and stakeholders within them.

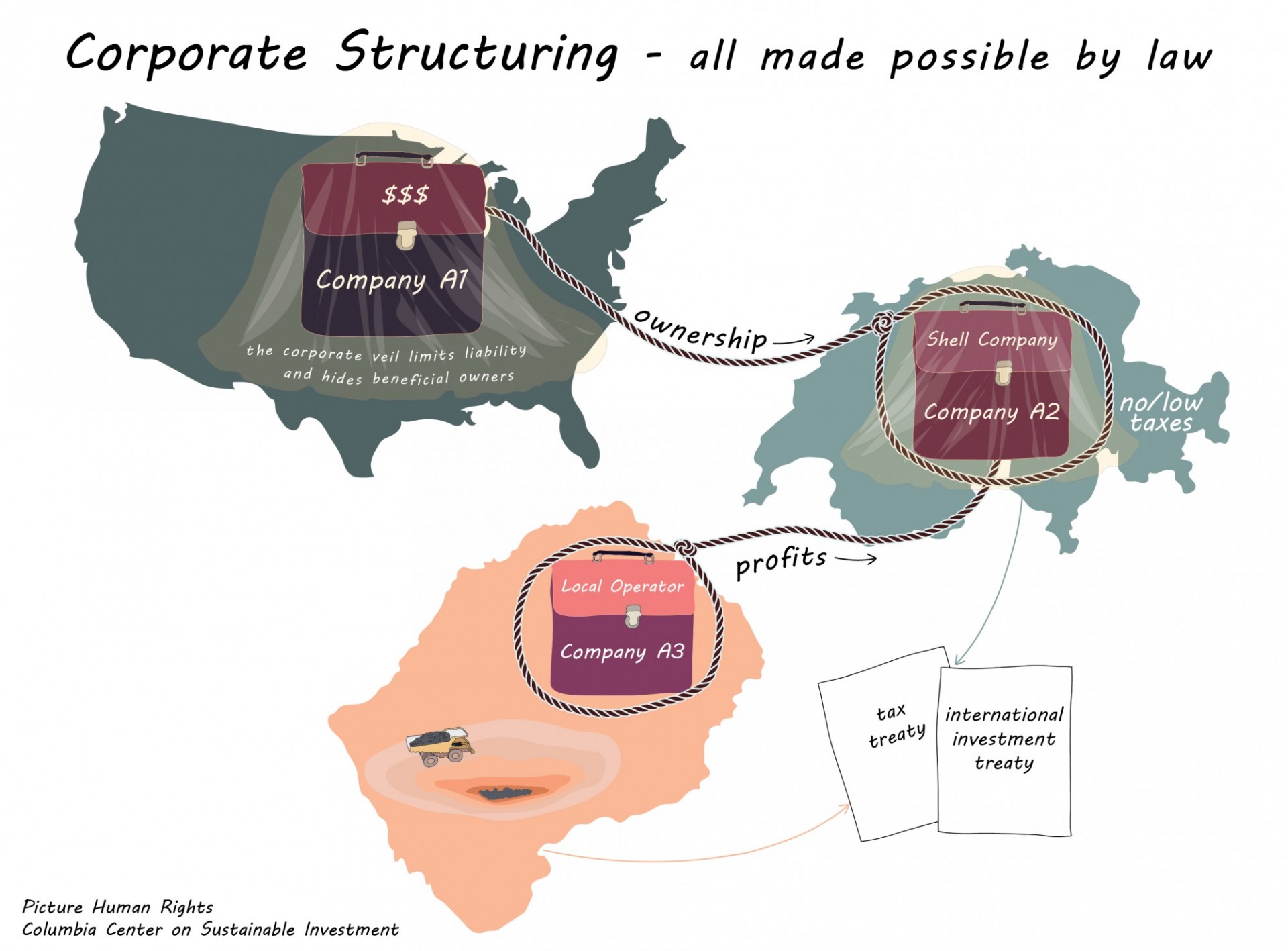

While there is no clear evidence that IITs stimulate new investment flows, they may affect how investments are structured. This is because arbitrators have interpreted treaties to allow investors to bring claims though subsidiaries and holding companies located in treaty parties.

What privileges do IITs provide to investors? IITs typically require states to provide foreign investors certain standards of treatment. Provisions include:

- Requirements to compensate investors in the event of direct or indirect expropriations,[2]

- Protections against treatment by government actors that tribunals deem to be “unfair” or “inequitable,” which have been interpreted to cover investors’ “legitimate expectations” about future business activities and government conduct, and

- Protections against “discrimination,” which have been interpreted to prevent disparate treatment even in the absence of nationality-based discrimination.

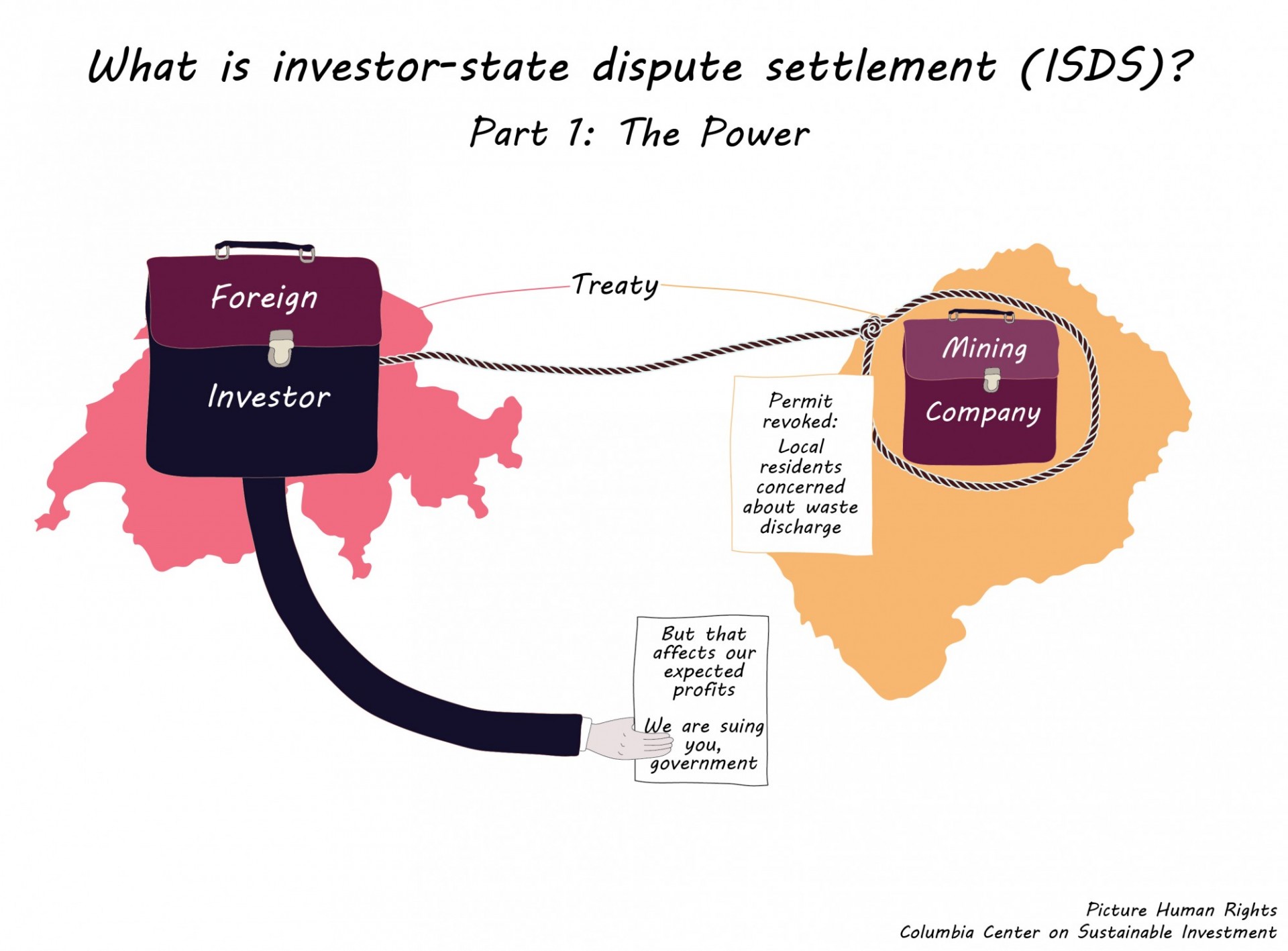

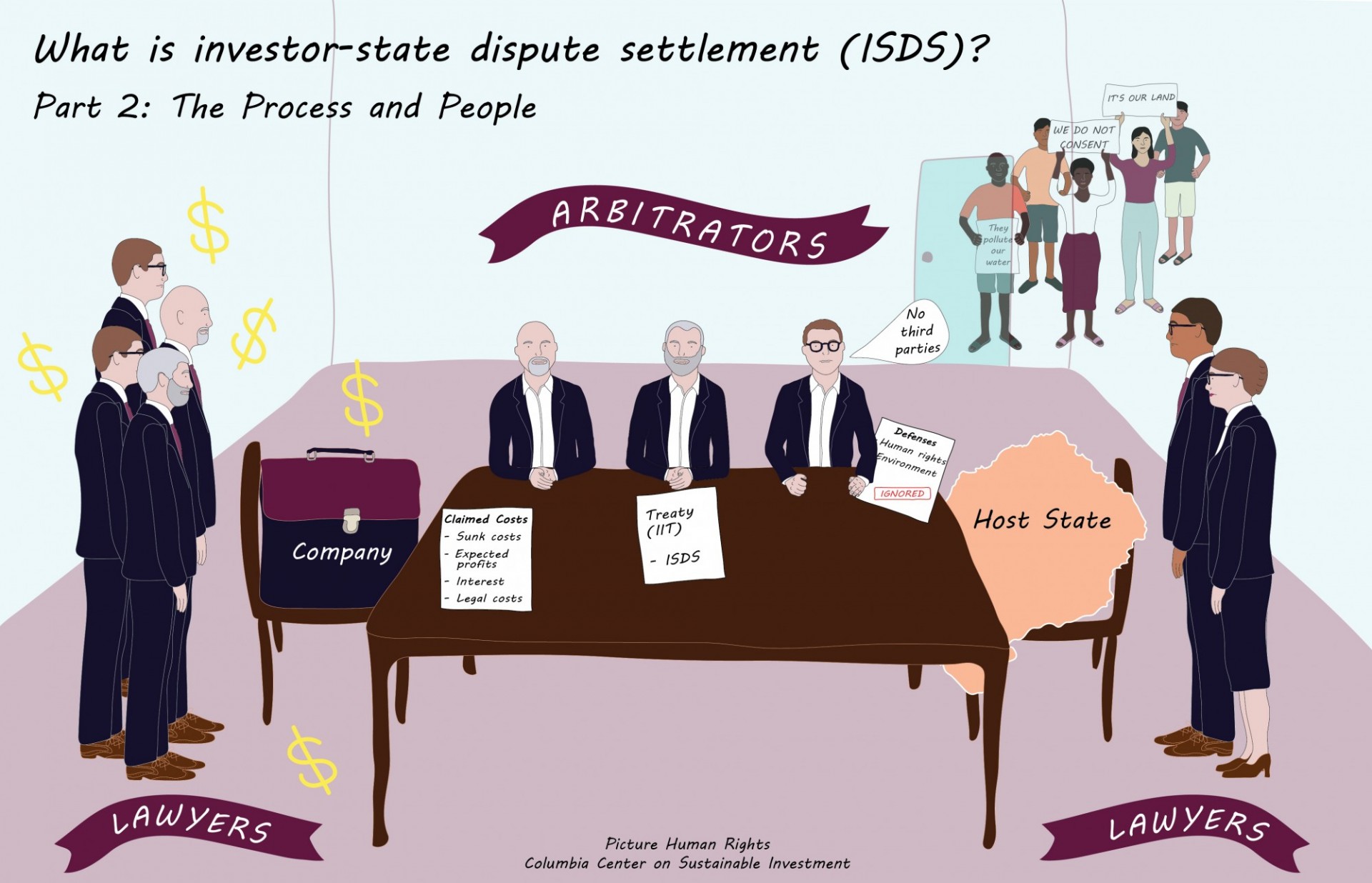

What is Investor-State Dispute Settlement (ISDS)? IITs allow foreign investors (individuals and companies)[3] to allege treaty violations by suing states through arbitration. Arbitration tribunals are appointed and paid for by one or both of the disputing parties. Tribunals are not bound by precedent, and can order remedies (usually in the form of monetary awards) to investors if they find that states have breached treaty obligations. In most cases, investors are not required to attempt to resolve disputes through available domestic remedies before filing ISDS claims. This is extraordinary and unusual: by contrast, the WTO only permits states to raise claims against other states, and international human rights courts require claimants to attempt to exhaust domestic remedies before raising disputes at the supranational level.

How does ISDS affect states’ ability to govern? One way of thinking about the treaties is that they provide internationally enforceable substantive protections for covered investors’ economic rights and interests that are akin to the “Lochnerism” of the US Supreme Court until the 1930s. This approach privileges the economic rights and interests of international investors/multinational enterprises (MNEs) over competing economic and non-economic interests of other entities and individuals. (Distinct from Lochnerism, however, where the US Supreme Court was able to shift course, it is particularly difficult to course-correct in a fragmented and often conflicted international investment law regime that lacks meaningful checks and balances). The deferential treatment afforded to economic interests increases the cost of regulating, and as the United States Trade Representative acknowledged, may even chill good faith action in the public interest.

Cases have been brought against states to challenge myriad actions, including, among other things:

- Efforts to combat tax evasion and money laundering;[4]

- Efforts to strengthen environmental laws or enforcement thereof;[5]

- Efforts to address climate change and limit extraction of fossil fuels;[6]

- Government regulation of the price and quality of essential public services such as provision of water and energy;[7]

- Government regulation of health care products and services;[8]

- Government efforts to set intellectual property protections at a level that balances private and public needs;[9]

- Government initiatives to try to mitigate the effects of historic discrimination;[10] and

- Government efforts to ensure foreign investment catalyzes domestic development.[11]

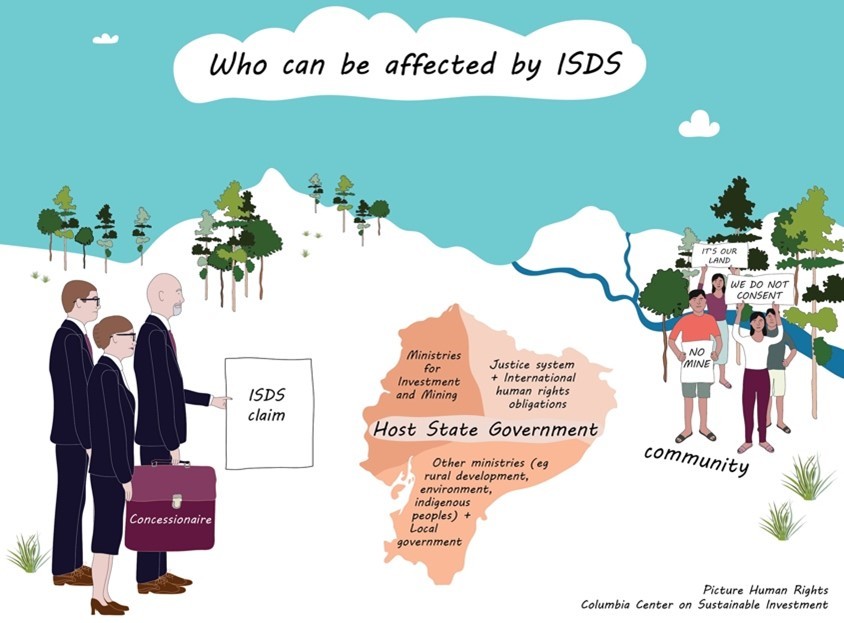

How are the rights of third-parties impacted by ISDS disputes? ISDS proceedings are generally opaque, secretive, and exclusive compared to the US and other domestic legal systems, which are more transparent and have mechanisms to consider and safeguard the rights and interests of non-parties. ISDS tribunals have discretion to accept, or not, third-party amicus briefs, but frequently reject (see here and here) or place significant restraints on them, even when the rights or interests of non-parties are directly at stake in the ISDS claim. Unlike common legal protections that allow affected non-parties to participate in cases (e.g. as impleaders or interpleaders), and/or require cases to be dismissed if third-parties will be affected but cannot join the proceedings, affected third parties in ISDS have no clear ability to effectively intervene in an ISDS proceeding, and there are no rules providing for ISDS cases to be dismissed when those cases threaten third-parties’ rights.

Governments recently affirmed that international reform efforts should address concerns that the rights or interests of third parties can be affected by ISDS disputes. But there are no concrete plans in place to advance or implement those reforms.

How many cases have there been? Through the end of 2018, at least 1104 cases had been filed.[12] There has been a rapid proliferation of these cases in recent years; while the first ISDS case was initiated in 1987, over half of all cases to date were filed between 2013 and 2021.

Who usually brings ISDS cases? Who usually defends them? Successful claims are often brought by large multinational corporations: companies with over US$1 billion in annual revenue and individuals worth more than US$100 million have received about 94.5% of the aggregate ISDS-ordered financial transfers (93.5% if pre-award interest is included). The vast majority (86%) of investor claimants are from high-income countries, whereas the majority (66%) of cases are against lower and middle-income countries. Particularly, in lower-income countries, ISDS losses can have a significant economic impact.

Who decides cases? ISDS cases are typically decided by panels of three arbitrators, appointed and paid for by the investor and the respondent state (one arbitrator is typically selected by each party and one selected jointly). Arbitrator selection is generally not subject to any qualification requirement (e.g. related to areas of expertise), nor meaningful guarantees of independence. A small pool of arbitrators are appointed and reappointed in the vast majority of cases. Some arbitrators also “double-hat,” representing claimants in ISDS disputes while also sitting as arbitrators in other cases. This can and has led to scenarios in which attorneys have used awards they have issued as arbitrators to support their legal positions when arguing as counsel. In addition, some counsel and arbitrators are paid as experts in other disputes, or as advisors to third-party funders of arbitration claims. (As noted below, the European Union is currently leading an effort to replace party-appointed and party-paid arbitrators by a standing body or roster of adjudicators. There are also some efforts to limit “double-hatting” in treaties currently under negotiation as well as through the ISDS reform process taking place through the United Nations Commission on International Trade Law. The content and take-up of those possible reforms, however, remain uncertain.)

What do arbitrators consider in deciding cases? Arbitral tribunals look first and foremost at the provisions of the relevant investment treaty in deciding cases. Whether or not a challenged governmental action (or inaction) is consistent with domestic law or other areas of international law (e.g. UNFCCC, human rights frameworks, etc.) is generally not considered to be a defense to claims or liability under the IIT (but a breach of those other sources of law may be deemed to violate the IIT). Conversely, because treaties almost universally place enforceable obligations only on states, not investors, meaning that states can generally not initiate claims nor bring counterclaims in ISDS, an investor may win a case even if it has violated domestic law or other international human rights or environmental norms in relation to its operation of the investment. To influence interpretation, the state defending itself, as well as the other state party or parties to the treaty (including the investor’s home state) can offer joint (and unilateral) interpretations to clarify what treaty provisions mean. But what a respondent state says about the meaning of the treaty is often discounted by tribunals. Indeed, even when all treaty parties agree on the proper interpretation of the treaty, tribunals have departed from that interpretation in favor of their own. Tribunals may, and often do, draw from prior ISDS decisions but are not bound by precedent.

[Zoom in on “ignored” “Defenses” in illustration above]

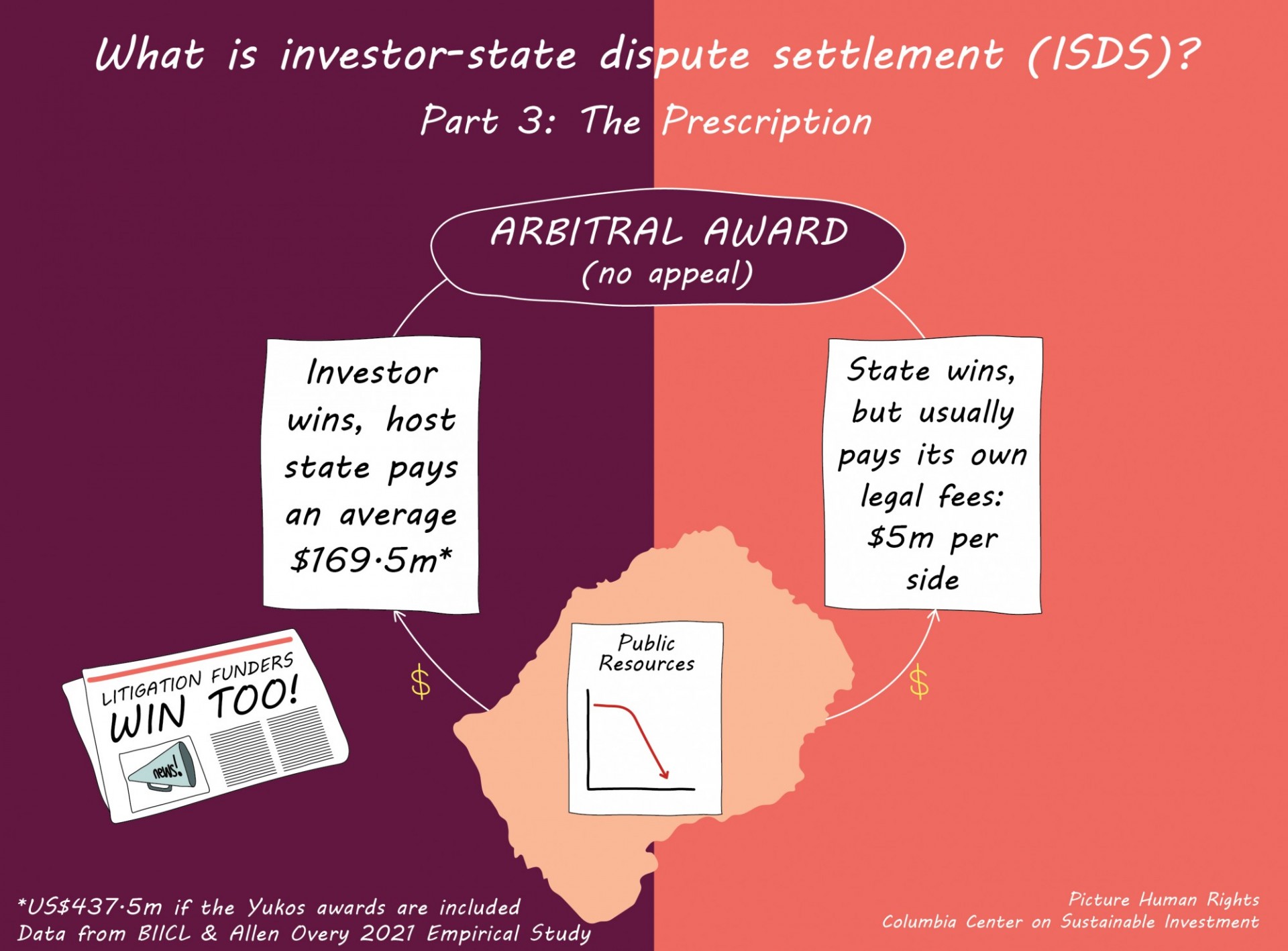

What happens when investors win cases? ISDS tribunals do not generally mandate specific performance; that is, they do not overturn or require reversal of state conduct. Instead, they typically award monetary damages to investors (even in cases where monetary damages would not be a permissible remedy under comparable domestic law, where remand or other equitable remedies may apply). But the line between specific and monetary relief has become increasingly blurred. Tribunals have, for instance, ordered injunctive relief against states (e.g., telling the executive to halt tax collection efforts, cease criminal proceedings, and preclude enforcement of domestic court judgments) and have then found states monetarily liable for government decisions not to comply with those tribunal orders (e.g., here). Awards against states regularly climb into the hundreds of millions of dollars, and have reached billions of dollars. As of June 2021, the average amount sought by investors in each ISDS claim is US$1.16 billion.[13] The average amount states are ordered to pay is US$437.5 million.[14] The same study from 2021 also finds that, excluding the Russian outliers, both the average amount claimed and average amount awarded are increasing. Indeed, between 2017-2020, tribunals ordered governments to pay an average of US$315.5 million each time they were successfully sued.

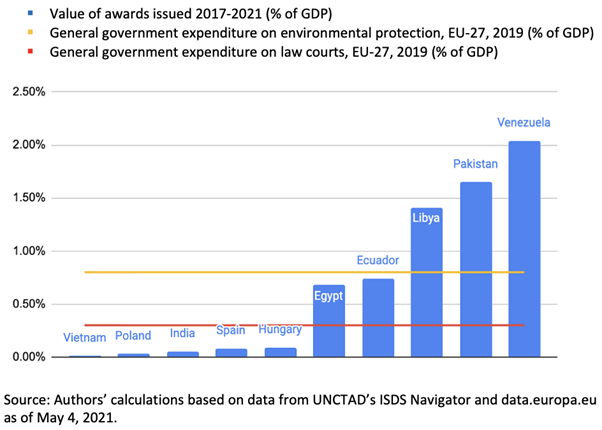

Low- and middle-income countries are often subject to awards that consume large portions of their annual budgets (i.e., resources that could otherwise be spent on health, education, and other national priorities).

The chart below shows the value of awards issued over the past five years against ten respondent states as a percentage of GDP, and illustrates the amount of those awards relative to EU states’ expenditures (as a percentage of GDP) on other public programs.

Awards are highly enforceable and cannot be “appealed” as such, even if the ISDS tribunal made a mistake in interpreting or applying the law, or in its understanding of the facts. If states do not pay the awards, and the investors face trouble enforcing awards through, e.g., seizure of government assets, investors may try to get their “home” states to place diplomatic pressure or impose penalties on the host government.[15]

What are costs to states of defending against these claims? The average ISDS proceeding costs around $13 million for the claimant and respondent combined, including tribunal costs. Complicated and high-stakes cases can cost more. In TCC v. Pakistan,[16] for example, Pakistan’s legal fees were nearly $25.5 million. It was also ordered to pay all of the over $59.5 million in legal costs incurred by the claimant, as well as the full amount of the arbitration fees, which was over $3.7 million. For states defending multiple claims in short order, these fees can add up — consider Colombia, where 17 cases (and counting) have been filed since 2016.

What is “Third-Party Funding” and why does it matter? Financial firms increasingly fund and even recruit investors to bring ISDS cases, covering the claimants’ legal costs in exchange for a stake in potential awards. This raises a number of questions, including whether the introduction of third-party funding leads to an increase in overall claims or amounts sought, an increase in “marginal” or frivolous claims, alters win-loss ratios, impacts legal outcomes and overall development of the law, and has broader effects on international flows of capital and taxation of that capital.

Third-party funding in claims against governments is currently almost entirely unregulated in investment arbitration. This contrasts with approaches taken in at least some countries at the domestic level, where policy considerations limit the use of third-party funding in lawsuits against the government. In the US, for example, the Anti-Assignment of Claims Act,[17] prohibits “a transfer or assignment of any part of a claim against the United States Government or of an interest in a claim,” as well as “authorization to receive payment for any part of the claim.” There are exceptions, such as permitting interest in claims to be transferred after those claims have been determined to be valid and after the amount owed has been decided.

The Anti-Assignment aims to serve several policy objectives:

first, to prevent persons of influence from buying up claims which might then be improperly urged upon Government officials; second, to prevent possible multiple payment of claims and avoid the necessity of the investigation of alleged assignments by permitting the Government to deal only with the original claimant; and third, to preserve for the Government defenses and counterclaims which might not be available against an assignee.[18]

Those policy objectives are not protected under the current laissez-faire approach to third-party funding in ISDS.

What now? Approaches to reform:

A number of states are considering various ISDS reforms and new IIT models, and are crafting new treaties that aim to address at least some of the recognized problems. Importantly, UNCITRAL’s Working Group III — the first major multilateral negotiations on investment that have occurred since the OECD’s failed attempt in the mid-1990s to establish a Multilateral Agreement on Investment — is also pursuing ISDS reform.

UNCITRAL’s efforts include at least some further work on the European Union’s proposed multilateral investment court, which suggests swapping party-appointed and party-paid arbitrators with more permanent salaried ‘judges’ as a way of addressing some problems with ISDS. However, this will not, on its own, address many of the aforementioned issues with ISDS, such as those related to the substantive scope and potential regulatory chill of IITs. Indeed, it may even lock in the legal interpretations and types of damage awards that threaten to unduly thwart or increase the cost of public interest regulation, or shift those costs to the public in ways inconsistent with the “polluter pays” principle or other equitable considerations. It is also unclear whether the proposal for a multilateral court will attract enough signatories, or the right signatories, to make a difference for countries defending claims.

For the most part, however, all reform efforts have focused on relatively small changes to ISDS and have not considered more fundamental reforms to shift course on an IIT/ISDS system increasingly considered to be ineffective, lack legitimacy, and have unintended and undesirable effects on other regulatory prerogatives.

At CCSI, we contend that it is important to more broadly assess the costs and benefits of investment treaties and ISDS, and rethink the role of international investment agreements as tools for advancing sustainable development, from home and host country perspectives. This means looking more closely at the objectives of these agreements, and at how IITs may better align with the Sustainable Development Goals, as well as at alternative modes of dispute settlement that might better serve identified objectives.

While reforms are being discussed, investors will continue to bring, and states will continue to defend, claims in an ISDS system now widely recognized as suffering from perceived and actual concerns going to its very legitimacy. CCSI is therefore exploring shorter-term ways for states to exit or mitigate the recognized adverse effects of the more than 3,300 treaties that have been concluded to date. Chief among these options, we’ve advocated for termination (or withdrawal of consent to ISDS arbitration) of these treaties, as a near-term solution, alongside any longer-term project.

[1] Another 2020 meta-analysis of 40 empirical studies estimated that the impact of IITs on increases in FDI was below 1% overall when accounting for publication bias in existing studies.

[2] Indirect expropriations are defined as one or a series of government measures that substantially deprive investors of the value of their investments.

[3] Protected investors can include not only a multinational enterprise (MNE) headquartered in a state party to the treaty, but also a subsidiary established in a treaty party, debt or equity investors, holders of IP rights, third party funders who invest in companies to assume ISDS privileges, and other individuals and entities.

[4] See, e.g., Federal Elektrik Yatirim v. Uzbekistan, ICSID Case No. ARB/13/9; Quiborax v. Bolivia, ICSID Case No. ARB/06/2, Award, 16 September 2015.

[5] See, e.g., Glamis Gold Ltd. v. United States, Award, 8 June 2009; Lone Pine Resources v. Canada, ICSID Case No. UNCT/15/2 (UNCITRAL); Vattenfall AB, Vattenfall Europe AG, Vattenfall Europe Generation AG v. Germany, ICSID Case No. ARB/09/6; Gabriel Resources v. Romania, ICSID Case No. ARB/15/31; Clayton/Bilcon v. Canada, PCA Case No. 2009-04, Award on Jurisdiction and Liability, 17 March 2015, and Award on Damages, 10 January 2019.

[6] See, e.g., RWE v. the Netherlands, ICSID Case No. ARB/21/4; Uniper v. the Netherlands, ICSID Case No. ARB/21/22; Rockhopper v. Italy, ICSID Case No. ARB/17/14; TransCanada v. USA, ICSID Case No. ARB/16/21; Westmoreland v. Canada, ICSID Case No. UNCT/20/3; Lone Pine v. Canada, ICSID Case No. UNCT/15/2.

[7] See, e.g., United Utilities (Tallinn) B.V. and Aktsiaselts Tallinna Vesi v. Estonia, ICSID Case No. ARB/14/24; Suez, Sociedad General de Aguas de Barcelona, S.A. and Vivendi Universal, S.A. v. Argentina, ICSID Case No. ARB/03/19, Award, 9 April 2015; TECO Guatemala Holdings, LLC v. Guatemala, ICSID Case No. ARB/10/23, Award, 19 December 2013, and Decision on Annulment, 5 April 2016.

[8] See, e.g., Achmea B.V. v. The Slovak Republic, PCA Case No. 2013-12 (UNCITRAL); HICEE B.V. v. The Slovak Republic, PCA Case No. 2009-11 (UNCITRAL), Final Award, 17 October 2011; Apotex Holdings Inc. and Apotex Inc. v. United States of America, ICSID Case No. ARB/AF/12/1, Award, 25 August 2014.

[9] See, e.g., Eli Lilly and Company v. Canada, ICSID Case No. UNCT/14/2 (UNCITRAL), Final Award, 16 March 2017.

[10] See, e.g., Piero Foresti, Laura de Carli & Others v. South Africa, ICSID Case No. ARB(AF)/07/1, Award, 4 August 2010.

[11] See, e.g., Mobil Investments Canada Inc. and Murphy Oil Corporation v. Canada, ICSID Case No. ARB(AF)/07/4.

[12] However, not all cases or filings are public because rules requiring transparency are not consistently adopted or applied. Disputing parties, and/or the arbitrators, could still decide to try to keep the arbitrations partially or totally confidential, though in such cases, journalists and other may try to use Freedom of Information laws to try to access the relevant information.

[13] Removing a set of particularly large claims against Russia for tens of billions of dollars, the average amount sought in each case is US$817.3 million.

[14] Removing the awards against Russia, which are particularly large outliers ordering that government to pay US$50 billion to investor claimants, the average ISDS award is US$169.5 million.

[15] For example, following Argentina’s failure to comply with several awards issued to U.S. investors between 2000 and 2008, the U.S. government withdrew trade benefits allowed to Argentina as a beneficiary developing country under the U.S. Generalized System of Preferences, and voted against the extension of loans to the country by the World Bank and Inter-American Development Bank. Emmanuel Gaillard, Ilija Mitrev Penushliski, ‘State Compliance with Investment Awards,’ (2021) ICSID Review – Foreign Investment Law Journal.

[16] Tethyan Copper Company v. Pakistan, ICSID Case No. ARB/12/1, Final Award, 12 July 2019.

[17] 31 USC § 3727

[18] Kingsbury v. United States [1977] 563 F.2d 1019, 1024.